Sponsored Article

Money in the UAE moves fast. Salaries, land rent hits, school fees pop up, and data plans renew. In Dubai, a teacher stretches AED through the month; one slip and late fees bite. A stray tap on a fake link and a card lock. Plans change, day gone. Navigating these financial obligations becomes even more crucial for those relying on banking services for expatriates in uae. With so many options available, it’s essential to choose wisely to avoid unexpected charges and ensure money transfers are seamless. Each month, the same routine begins, but the stakes feel higher, as the fast-paced lifestyle can quickly lead to financial missteps. It’s vital to stay informed about the latest updates, such as the emirates nbd remittance fee changes, which can impact the overall budgeting process. Regularly reviewing financial commitments and services can help mitigate the risks of incurring unnecessary costs. As the month draws to a close, prioritizing financial literacy becomes essential to maintain stability amidst the flowing tides of expenses.

This page stays practical. It lists tools to use now on budgeting that actually stick, bank app controls that reduce mistakes, and the basics of your AECB credit score. It also maps real protection routes: how to freeze a card, report fraud, and file a complaint with the Central Bank of the UAE. Clear steps, short lists, useful links. Additionally, it explores alternative investment options in finance that can help diversify your portfolio and mitigate risks. These options are complemented by practical advice on how to assess their potential returns and associated risks. Ultimately, this guide aims to empower individuals with the knowledge they need to take control of their financial futures.

Tools You Can Use Today

Start simple. List fixed bills first: rent, transport, school fees, data plans. Then note flexible spends: groceries, eating out, streaming. Use a tracker that tags AED by category and pulls bank transactions cleanly. Color helps. So do weekly check-ins. Consider setting aside a portion of your income for savings and emergencies to ensure financial stability. If you’re looking for a flexible but efficient way to manage your finances, you might want to open emirates nbd salary account, which offers tools and features tailored for tracking expenses. Additionally, reviewing your budget monthly can help you identify areas for improvement and make adjustments as needed. Integrating a balance check for salary card into your routine can provide real-time insights into your spending and savings progress. This practice can enhance your budgeting efforts and ensure you are always aware of your financial standing. Regularly updating your financial goals based on your budget review can also lead to more strategic spending and saving behaviors.

When overdue notices pile up, learn the order in which things move. For debts that enter formal collection, review the process with Qlegal Consultancy to understand notices, timelines, and options in the UAE. For complex disputes, collect plain records—dates, amounts, screenshots—and line up solid legal advice before anything escalates. Stay informed about external factors that could impact your financial situation, such as fluctuations in gold prices in uae on october 20. Keeping abreast of these changes can help you make strategic decisions regarding your debts. Additionally, consider seeking financial counseling for a comprehensive approach to managing your obligations. Utilizing tools such as a ‘lulu salary card balance check‘ can help you monitor your finances more effectively. This allows you to make timely payments and manage your budget better as you navigate your debt obligations. Regularly assessing your financial standings empowers you to prioritize which debts to address first, ensuring you maintain control over your financial health.

Bank App Safety and Controls

Most UAE banking apps carry strong tools. Turn on instant alerts for every card and account.

Use controls: freeze or unfreeze, set per-transaction limits, and block international or contactless when you don’t need them. Create a virtual card for online purchases. Name savings pockets—rent, school, visa fees—so money has a job. Check ATM and FX fees before travel; those add up on busy Dubai weekends. Consider setting up alerts for your transactions to monitor spending and ensure you stay within your budget. If you’re looking for a convenient way to manage funds, learn how to open du pay account to simplify your finances. Additionally, always review your expenses regularly to identify areas where you can save or adjust your spending habits. As you optimize your finances, stay updated on any changes in policies, such as the uae banks minimum balance increase, which could impact your budgeting strategies. Regularly revisiting your savings goals and adjusting them based on current financial obligations can also lead to better results. Don’t hesitate to explore different banking services that may offer enhanced features catering to your needs.

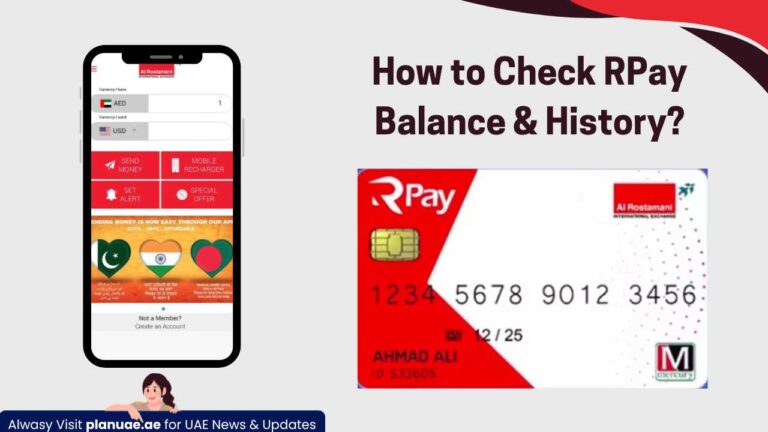

If a payment goes sideways, act fast. Freeze the card, note the time, and contact the bank through the app chat or hotline. Keep the case number. If the issue looks legal, seek legal guidance early and save every message. Consider reviewing your recent transactions to identify any unauthorized charges, which can help your bank resolve the issue more efficiently. Additionally, explore the ppc fab bank balance methods to ensure you’re managing your funds effectively while the situation is being addressed. Staying organized and proactive can make a significant difference in resolving payment disputes. In parallel, familiarize yourself with the rpay balance enquiry process to keep track of your available funds and prevent any surprises. Being aware of your balance allows you to manage your finances while the dispute is resolved. Remember, thorough documentation and timely action are key to a successful resolution.

Know Your Credit Standing (AECB)

The AECB score sums up payment habits in the UAE. On-time bills build trust; missed ones cut it. Pull the score before a new card, car loan, or plan. Read the report, not just the number. Late utilities, bounced checks, and high utilization all leave marks. Understanding your AECB score can help you make informed financial decisions and improve your overall creditworthiness. If you’re unsure about how to check your credit score, there are online platforms and services specifically designed to provide you access to your report. Regularly monitoring your score can help you identify areas for improvement and ensure better chances for approval on future loans or credit applications. Additionally, it’s essential to stay informed about the know your customer regulations in uae as these can impact your credit applications and overall financial dealings. Familiarizing yourself with these regulations can help you build a stronger financial profile and navigate the lending landscape with greater confidence. By being proactive in managing your credit and understanding the legal framework, you can enhance your chances of securing financing when needed.

To lift a weak score, pay on time, and more than the minimum. Keep card balances far below limits. Avoid opening several lines at once. If a collector calls on an old balance, ask for written details. Before signing any settlement, get legal rights advice so the terms don’t backfire. When a claim heads toward court, prepare to get legal representation and keep documents tidy. Additionally, it’s crucial to monitor your credit reports regularly to ensure accuracy and catch any discrepancies early. Understanding how to check ratibi card balance can also help you manage your finances more effectively and avoid any unnecessary fees. By staying informed and proactive, you can improve your credit profile over time.

Protection and Complaint Routes

Scams often start the same way: “account blocked” calls, prize texts, rushed payment links. Hang up. Don’t tap. Open the bank app, check activity, and turn on alerts. Save screenshots and note times—clean evidence helps later. Stay informed about the latest scams and security measures. The UAE Central Bank AML crackdown is strengthening oversight to combat fraud, so report any suspicious activities promptly. Sharing your experiences with friends and family can also help protect them from becoming victims. Additionally, if you’re looking to sever ties with banking services that may no longer meet your needs, it’s essential to understand the process involved, such as how to close Mashreq Neo account. Ensure that you retrieve all necessary documents and settle any outstanding transactions before proceeding. Staying vigilant and informed can significantly reduce your chances of falling victim to future scams.

Move in order when fraud hits:

- Freeze the card and change the PIN.

- Call the bank from the number in the app; ask for a dispute case and write the ID.

- Disable risky features you don’t need today.

- Report cyber issues through the UAE’s eCrime portal and log spam with your telecom.

- Track everything in one note: dates, amounts, reference numbers. If the dispute gets messy, line up legal guidance and store copies of every document.

If a dispute stalls, take it to the Central Bank’s consumer channels. Prepare a short pack: Emirates ID, masked account or card numbers, statements, screenshots, and the bank’s case ID. State the facts in plain words—what happened, what you requested, what the bank offered. Once your case is submitted, be patient and follow up periodically to ensure it is being addressed. Additionally, while navigating financial matters, you might also want to research how to verify medical insurance status to ensure your coverage is active and adequate. This can help prevent any unexpected issues should you need medical assistance during the dispute process. Additionally, it’s important to keep track of other financial aspects, such as your transportation expenses. Knowing how to check hafilat card balance can help you manage your travel costs effectively during this time. Staying organized with your finances will allow you to focus on resolving the dispute without added stress.

Quick Tips

- Set bill reminders two days early.

- Use virtual cards for online buys; keep limits tight.

- Keep one running note with case IDs, dates, and screenshots.